Many consumers across the United States, United Kingdom, Canada, Germany, France, Japan, and Australia face a common decision when getting a new vehicle. Should they finance the car with a loan or should they lease it? The answer can mean a difference of thousands of dollars over three years. This article compares the total costs of buying with a loan versus leasing using actual dollar amounts based on 2026 market rates. It is for informational and educational purposes only.

How Car Loans Work

A car loan allows the borrower to purchase the vehicle and own it after the loan is repaid. The lender provides a lump sum to pay for the car. The borrower repays the loan in fixed monthly installments over a set term typically 36, 48, or 60 months. Interest rates in 2026 for borrowers with good credit range from 6 percent to 12 percent APR. The borrower owns the vehicle from day one but the lender has a lien until the loan is paid off.

How Car Leases Work

A car lease is essentially a long term rental. The lessee pays for the depreciation of the vehicle during the lease term plus interest and fees. The lessee does not own the vehicle. At the end of the lease term typically 24 to 48 months, the vehicle is returned to the dealership. The lessee can also choose to buy the vehicle at the residual value. Monthly lease payments are typically lower than loan payments for the same vehicle because the lessee only pays for the portion of the vehicle value used during the lease term.

The Example Vehicle for This Comparison

To make a fair comparison, the same vehicle is used for both options. A 2026 mid size sedan with a purchase price of 35,000 dollars. The loan and lease are both for 36 months. The driver drives 12,000 miles or approximately 19,000 kilometers per year which is standard for most developed economies. The borrower has good credit and qualifies for competitive rates.

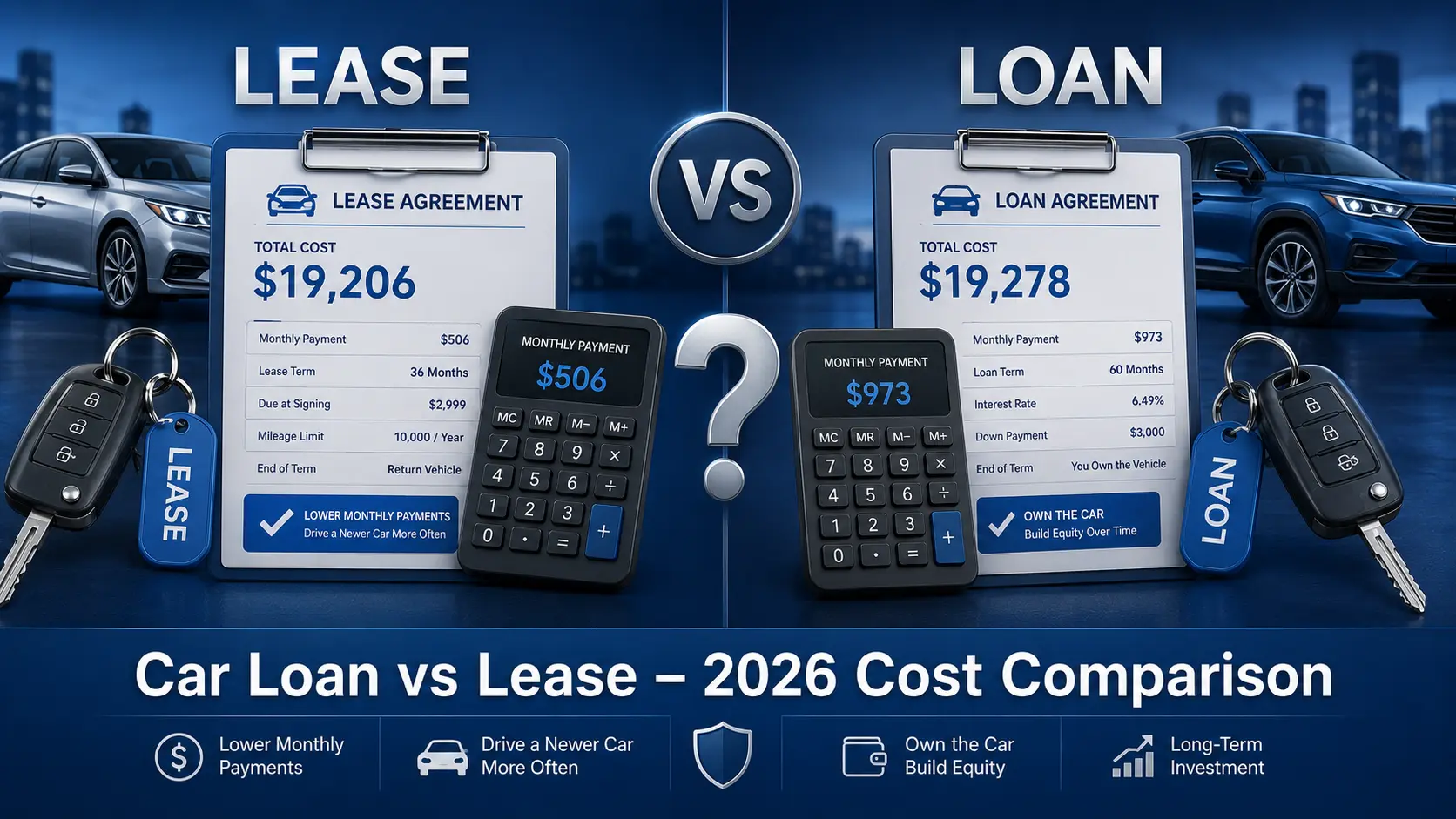

Total Cost of Buying with a Car Loan

For a 35,000 dollar car with a 10 percent down payment of 3,500 dollars, the loan amount is 31,500 dollars. With a 7 percent APR over 36 months, the monthly payment is approximately 973 dollars. Total payments over 36 months amount to 35,028 dollars. Adding the 3,500 dollar down payment brings the total paid to 38,528 dollars. After 36 months, the borrower owns the vehicle outright. The vehicle will have residual value. A 35,000 dollar car after 3 years and 36,000 miles typically retains approximately 55 percent of its original value. The resale value is approximately 19,250 dollars. If the borrower sells the car at the end of 36 months, the net cost of ownership is the total paid minus the resale value. That is 38,528 dollars minus 19,250 dollars equals 19,278 dollars.

Total Cost of Leasing the Same Vehicle

For the same 35,000 dollar vehicle over 36 months with 12,000 miles per year, the lease terms include several components. The capitalized cost is the negotiated price of 35,000 dollars. The residual value after 36 months is approximately 19,250 dollars or 55 percent of the original price. The depreciation cost is 35,000 dollars minus 19,250 dollars equals 15,750 dollars. The money factor or interest rate equivalent for a good credit lease in 2026 is approximately 0.0025 which is about 6 percent APR. The monthly depreciation cost is 15,750 dollars divided by 36 months equals 438 dollars. The monthly interest cost on the average of capitalized cost and residual value is approximately 68 dollars. The monthly payment for depreciation and interest is approximately 506 dollars. Additionally, most leases require an acquisition fee of approximately 595 dollars and a disposition fee of approximately 395 dollars at lease end. Upfront costs may include the first month payment and security deposit. Total monthly payments over 36 months at 506 dollars equal 18,216 dollars. Adding the acquisition fee of 595 dollars and disposition fee of 395 dollars brings the total to 19,206 dollars. The lessee does not own the vehicle at the end and has no resale value to recover.

Direct Dollar Comparison Over 36 Months

For the car loan scenario with sale at the end, the total cost is 19,278 dollars. For the lease scenario, the total cost is 19,206 dollars. The lease is only 72 dollars cheaper over three years. The difference is negligible. However, the loan scenario leaves the borrower with the option to keep the car for additional years with no monthly payments. The lease scenario requires returning the car and starting a new lease or purchase.

What Happens If the Borrower Keeps the Car Longer

If the borrower keeps the loan financed car for 60 months instead of selling at 36 months, the total cost changes. The monthly payment of 973 dollars over 60 months totals 58,380 dollars. Adding the 3,500 dollar down payment brings the total to 61,880 dollars. After 60 months, the vehicle is worth approximately 12,250 dollars or 35 percent of original value. The net cost of ownership over 5 years is 61,880 dollars minus 12,250 dollars equals 49,630 dollars. The average annual cost is 9,926 dollars. For a lease, the lessee would need to lease two more years with another vehicle. A second 24 month lease on a similar vehicle would cost approximately 11,000 dollars. Total lease cost over 5 years would be approximately 30,200 dollars with no asset at the end. Leasing becomes more expensive over longer periods.

Additional Costs for Both Options

Both loans and leases require insurance. Leases typically require higher coverage limits including higher liability and comprehensive coverage. Full coverage insurance on a leased vehicle can cost 1,200 to 1,800 dollars per year. A financed vehicle with a loan also requires full coverage but the owner may have more flexibility after the loan is paid. Maintenance costs are similar for both options. Leases require that the vehicle is maintained according to manufacturer schedule. Loans have the same requirement for owners who want to protect their asset.

Excess Mileage Charges on Leases

The example lease included 12,000 miles or 19,000 kilometers per year. If the driver exceeds this limit, excess mileage charges apply. Typical excess mileage fees are 15 to 30 cents per mile. Driving 15,000 miles per year instead of 12,000 adds 9,000 miles over three years. At 20 cents per mile, the excess fee is 1,800 dollars. This makes the lease significantly more expensive than the loan. The loan has no mileage restrictions.

Wear and Tear Charges on Leases

When returning a leased vehicle, the dealership inspects for excessive wear and tear. Normal wear is acceptable. Dents larger than a certain size, cracked windshields, stained carpets, or worn tires beyond normal limits can result in charges. A single damaged wheel can cost 500 dollars. Scratches requiring paint work can cost several hundred dollars. These charges can add 500 to 2,500 dollars to the lease end cost. Loan owners can sell the car with normal wear without penalty or repair issues before selling.

Upfront Cash Required for Both Options

The loan requires a down payment. For the example, 3,500 dollars or 10 percent down was used. Some loans allow zero down payment but interest rates are higher. The lease requires first month payment, acquisition fee, and security deposit. Upfront cash for the lease example is approximately 506 dollars first payment plus 595 dollar acquisition fee plus 500 dollar security deposit for a total of 1,601 dollars. The lease requires less upfront cash than the loan.

Real Dollar Examples for Different Vehicle Prices

Example one: A 25,000 dollar economy car. Loan with 2,500 down at 7 percent over 36 months. Monthly payment 695 dollars. Total with down payment 27,520 dollars. Resale value after 3 years approximately 13,750 dollars. Net cost 13,770 dollars. Lease on same car with residual 55 percent. Depreciation 11,250 dollars. Monthly payment approximately 340 dollars. Total lease cost including fees approximately 13,000 dollars. Lease is 770 dollars cheaper for economy cars.

Example two: A 50,000 dollar luxury sedan. Loan with 5,000 down at 7 percent over 36 months. Monthly payment 1,390 dollars. Total with down payment 55,040 dollars. Resale value after 3 years approximately 27,500 dollars. Net cost 27,540 dollars. Lease on same car with residual 55 percent. Depreciation 22,500 dollars. Monthly payment approximately 680 dollars. Total lease cost including fees approximately 25,700 dollars. Lease is 1,840 dollars cheaper for luxury vehicles.

When a Loan Is Better

A loan is better if the driver plans to keep the vehicle for more than four years. Once the loan is paid off, the owner has no monthly payments while still having a usable vehicle. A loan is better for drivers who drive more than 15,000 miles or 24,000 kilometers per year. Mileage penalties on leases become expensive. A loan is better for drivers who prefer to customize their vehicles. Leases prohibit most modifications. A loan is better for drivers who do not want to worry about wear and tear charges at the end.

When a Lease Is Better

A lease is better if the driver wants lower monthly payments. The example lease payment of 506 dollars was almost half the loan payment of 973 dollars. A lease is better for drivers who like getting a new vehicle every two to three years. The lease makes the transaction simple with no need to sell the old vehicle. A lease is better for drivers who stay within the mileage limits and keep the car in good condition. A lease is better for business owners who can deduct lease payments as a business expense in many developed economies.

Hidden Costs to Watch For

Early termination fees on leases can be extremely high. Ending a lease after 12 months instead of 36 can cost thousands of dollars. Loans can be paid off early with minimal penalty. Gap insurance is often included in leases. For loans, gap insurance is recommended for drivers who put less than 20 percent down. If the car is totaled, gap insurance covers the difference between the insurance payout and the remaining loan balance. Gap insurance typically costs 500 to 1,000 dollars.

Final Thoughts

For the average driver who keeps a vehicle for three years and drives 12,000 miles annually, leasing and buying with a loan cost approximately the same. The difference in the examples was only 72 dollars over three years. The decision should be based on driving habits, how long the driver plans to keep the vehicle, and whether lower monthly payments or long term ownership is more important. Drivers should always calculate total costs in dollars before signing any agreement.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, legal, or professional advice. Interest rates, residual values, fees, and lease terms change frequently. The examples shown are based on typical 2026 rates and are for illustration only. Actual costs depend on individual credit profiles, vehicle models, and local market conditions. Readers should compare actual offers from multiple dealers and consult with a qualified financial advisor before making any vehicle financing decisions.