Many consumers across the United States, United Kingdom, Canada, Germany, France, Japan, and Australia face a common question. When they need to borrow money, should they use a personal loan or a credit card? The answer can significantly affect how much interest they pay. A 10,000 dollar purchase financed incorrectly could cost thousands of dollars more than necessary. This article compares the costs of personal loans and credit cards using actual dollar amounts based on 2026 market rates. It is for informational and educational purposes only.

The Basic Difference Between Personal Loans and Credit Cards

A personal loan provides a lump sum of money that is repaid in fixed monthly installments over a set term. Interest rates are typically fixed. Once the loan is repaid, the account is closed. A credit card provides a revolving line of credit. The borrower can spend up to the credit limit, repay, and spend again. Interest accrues only on the unpaid balance. Minimum monthly payments are required but paying only the minimum extends the repayment period and increases total interest cost.

Typical Interest Rates in 2026

For borrowers with good credit scores of 670 or higher, personal loan rates in 2026 typically range from 7 percent to 15 percent APR. Credit card rates for the same borrower typically range from 18 percent to 25 percent APR. For borrowers with fair credit scores of 580 to 669, personal loan rates typically range from 18 percent to 30 percent APR. Credit card rates for fair credit often range from 25 percent to 32 percent APR. The rate difference alone makes personal loans cheaper for most borrowers who plan to repay over several months or years.

Comparing a 5,000 Dollar Borrowing Scenario

A consumer needs 5,000 dollars for a home repair. They compare a personal loan versus putting the expense on a credit card.

With a personal loan at 10 percent APR repaid over 24 months, the monthly payment is approximately 231 dollars. Total interest paid over two years is approximately 544 dollars. The total amount repaid is 5,544 dollars.

With a credit card at 22 percent APR, if the borrower pays 231 dollars per month the same as the loan payment, the credit card balance would be paid off in approximately 27 months. Total interest paid would be approximately 1,237 dollars. The total amount repaid would be 6,237 dollars.

The credit card costs 693 dollars more for the same 5,000 dollar borrowing amount. That is 127 percent more interest than the personal loan.

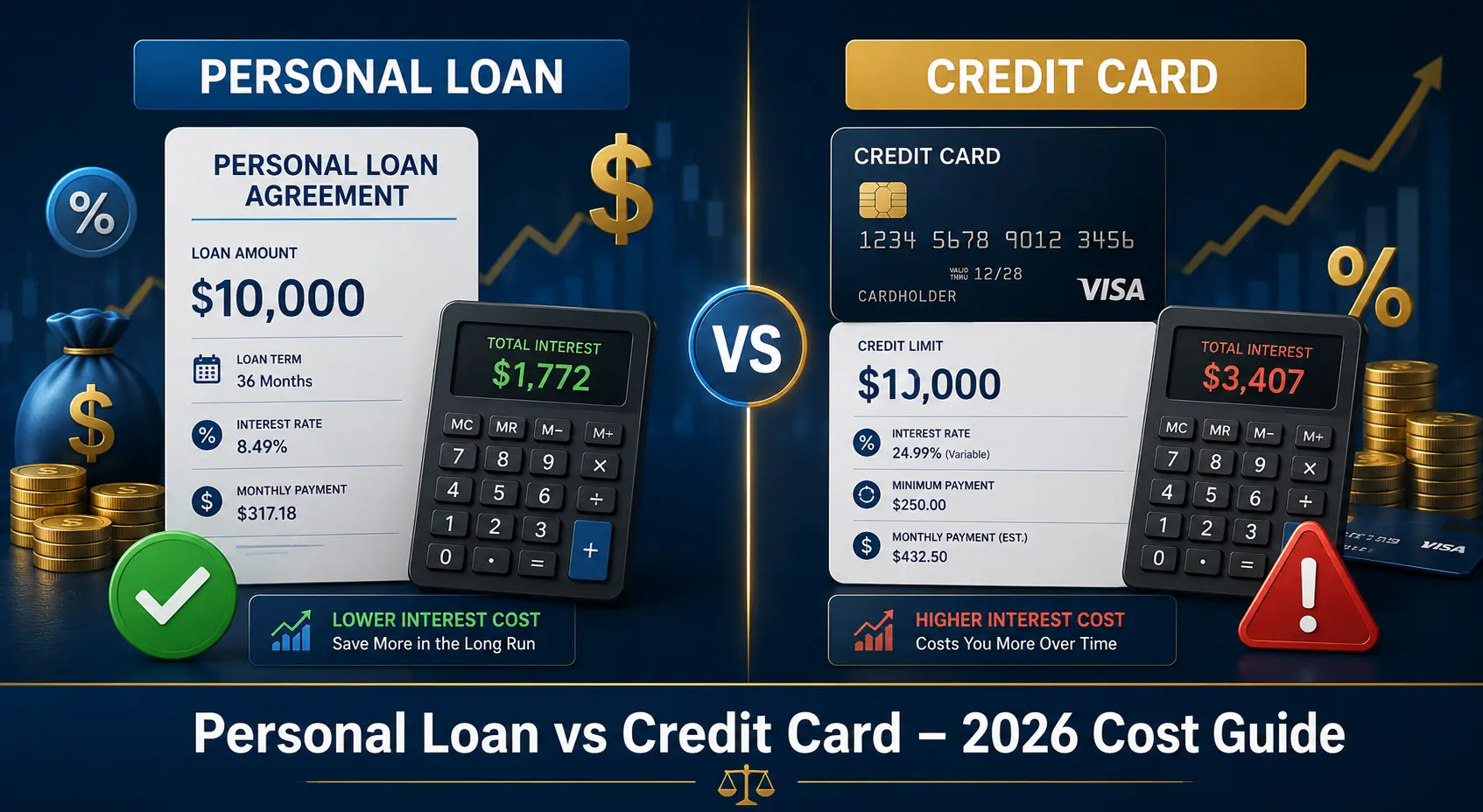

Comparing a 10,000 Dollar Borrowing Scenario

A consumer needs 10,000 dollars for a wedding or medical expense. They compare options over a 36 month repayment period.

With a personal loan at 11 percent APR over 36 months, the monthly payment is approximately 327 dollars. Total interest paid is approximately 1,772 dollars. Total amount repaid is 11,772 dollars.

With a credit card at 23 percent APR, making the same 327 dollar monthly payment, the balance would be paid off in approximately 41 months. Total interest paid would be approximately 3,407 dollars. Total amount repaid would be 13,407 dollars.

The credit card costs 1,635 dollars more for the same 10,000 dollar borrowing amount. This is nearly double the interest cost of the personal loan.

Comparing a 20,000 Dollar Borrowing Scenario

A consumer needs 20,000 dollars for debt consolidation or home improvement. They plan to repay over 48 months.

With a personal loan at 9 percent APR over 48 months, the monthly payment is approximately 498 dollars. Total interest paid is approximately 3,904 dollars. Total amount repaid is 23,904 dollars.

With a credit card at 20 percent APR, making the same 498 dollar monthly payment, the balance would be paid off in approximately 67 months. Total interest paid would be approximately 13,366 dollars. Total amount repaid would be 33,366 dollars.

The credit card costs 9,462 dollars more for the same 20,000 dollar borrowing amount. The credit card also takes 19 months longer to repay.

When a Credit Card Might Be Cheaper

A credit card can be cheaper than a personal loan in specific situations. If the borrower can pay the full balance within the grace period of 21 to 30 days, no interest is charged at all. A 500 dollar purchase paid in full by the due date costs zero interest on most credit cards. A personal loan would charge interest even for a short term loan.

Some credit cards offer introductory 0 percent APR periods for 12 to 21 months. A 3,000 dollar purchase financed on a 0 percent card costs zero interest if repaid before the promotional period ends. A personal loan for the same amount would cost several hundred dollars in interest.

Credit cards with rewards programs effectively reduce costs. A 2 percent cash back card on a 10,000 dollar purchase gives 200 dollars back. If the balance is paid immediately, the effective cost is negative 200 dollars.

Balance transfer credit cards offer low promotional rates. Some cards offer 3 percent to 5 percent one time fees with 0 percent APR for 12 to 18 months. For example, transferring 8,000 dollars with a 3 percent fee costs 240 dollars upfront. If repaid within 12 months, no additional interest is charged. A personal loan at 10 percent for 12 months would cost approximately 440 dollars in interest. The balance transfer card saves 200 dollars.

Hidden Costs to Watch For

Personal loans may have origination fees ranging from 1 percent to 8 percent of the loan amount. A 10,000 dollar loan with a 5 percent origination fee costs 500 dollars upfront. The borrower receives only 9,500 dollars but repays based on 10,000 dollars. This effectively increases the interest rate.

Credit cards may have balance transfer fees of 3 percent to 5 percent. Cash advance fees are typically 5 dollars or 5 percent of the amount whichever is greater. Cash advance interest rates are often higher than purchase rates and start accruing immediately with no grace period. Foreign transaction fees of 2 percent to 3 percent apply to purchases made outside the card’s home country.

The Minimum Payment Trap on Credit Cards

Credit cards allow very low minimum payments. A typical minimum payment is 1 percent to 3 percent of the balance or a fixed amount like 25 dollars whichever is greater. On a 10,000 dollar balance at 22 percent APR, paying only the 3 percent minimum of 300 dollars per month would take approximately 47 months to repay. Total interest would be approximately 4,100 dollars. The same 10,000 dollar personal loan at 11 percent over 36 months costs 1,772 dollars in interest. The credit card costs more than double when only minimum payments are made.

How Credit Scores Affect Both Options

A higher credit score qualifies for lower interest rates on both personal loans and credit cards. Improving a credit score from 650 to 750 can reduce a personal loan rate from 18 percent to 8 percent. On a 15,000 dollar loan over 48 months, that rate difference saves approximately 3,200 dollars in interest. For credit cards, the same score improvement can reduce APR from 28 percent to 18 percent. On a 5,000 dollar balance carried for 24 months, this saves approximately 500 dollars in interest.

Which One Is Right For Different Situations

For large expenses over 5,000 dollars that will take more than 12 months to repay, a personal loan is almost always cheaper. The fixed rate and fixed term provide predictable payments and lower total interest cost.

For small expenses under 1,000 dollars that can be repaid within one month, a credit card is cheaper if paid in full before the due date. No interest is charged at all.

For expenses between 1,000 and 5,000 dollars with repayment planned within 6 to 12 months, a 0 percent APR credit card is the cheapest option if available. After the promotional period ends, paying off the remaining balance quickly is important to avoid high rates.

For unexpected emergencies where immediate funds are needed and credit card limits are available, using a credit card temporarily while applying for a personal loan can work. The personal loan can then pay off the credit card balance, reducing the interest rate significantly.

Real Dollar Examples for 2026

Example one: A borrower needs 7,500 dollars for dental work. They can repay 400 dollars per month. A personal loan at 12 percent APR takes 21 months. Total interest is 903 dollars. A credit card at 24 percent APR takes 26 months. Total interest is 2,884 dollars. The personal loan saves 1,981 dollars.

Example two: A borrower needs 12,000 dollars for a used car. They can repay 500 dollars per month. A personal loan at 9.5 percent APR takes 26 months. Total interest is 986 dollars. A credit card at 21 percent APR takes 33 months. Total interest is 4,376 dollars. The personal loan saves 3,390 dollars.

Example three: A borrower finds a 0 percent APR credit card for 15 months with a 3 percent balance transfer fee. They need 6,000 dollars. The upfront fee is 180 dollars. Repaying 400 dollars per month clears the balance in 15 months with zero additional interest. Total cost is 6,180 dollars. A personal loan at 11 percent over 15 months costs approximately 495 dollars in interest. Total cost is 6,495 dollars. The credit card saves 315 dollars.

Final Thoughts

For most borrowing scenarios where repayment takes longer than a few months, personal loans cost significantly less than credit cards. The interest rate difference of 8 to 15 percentage points creates real dollar savings. However, credit cards can be cheaper for very short term borrowing or when promotional 0 percent APR offers are available. Consumers should always calculate the total interest cost in dollars before deciding which product to use.

Disclaimer : This article is for informational and educational purposes only and does not constitute financial, legal, or professional advice. Interest rates, fees, and terms change frequently. The examples shown are based on typical 2026 rates and are for illustration only. Actual rates depend on individual credit profiles. Readers should compare actual offers from multiple lenders and consult with a qualified financial advisor before making any borrowing decisions.